Users

Third-Party Payment Providers, End Customers, Compliance & Ops Team

Industry

Financial Services / Payments

Product Stage

Regulated, External-Facing Platform at Scale

Open Banking APIs & Third-Party Payments Enablement

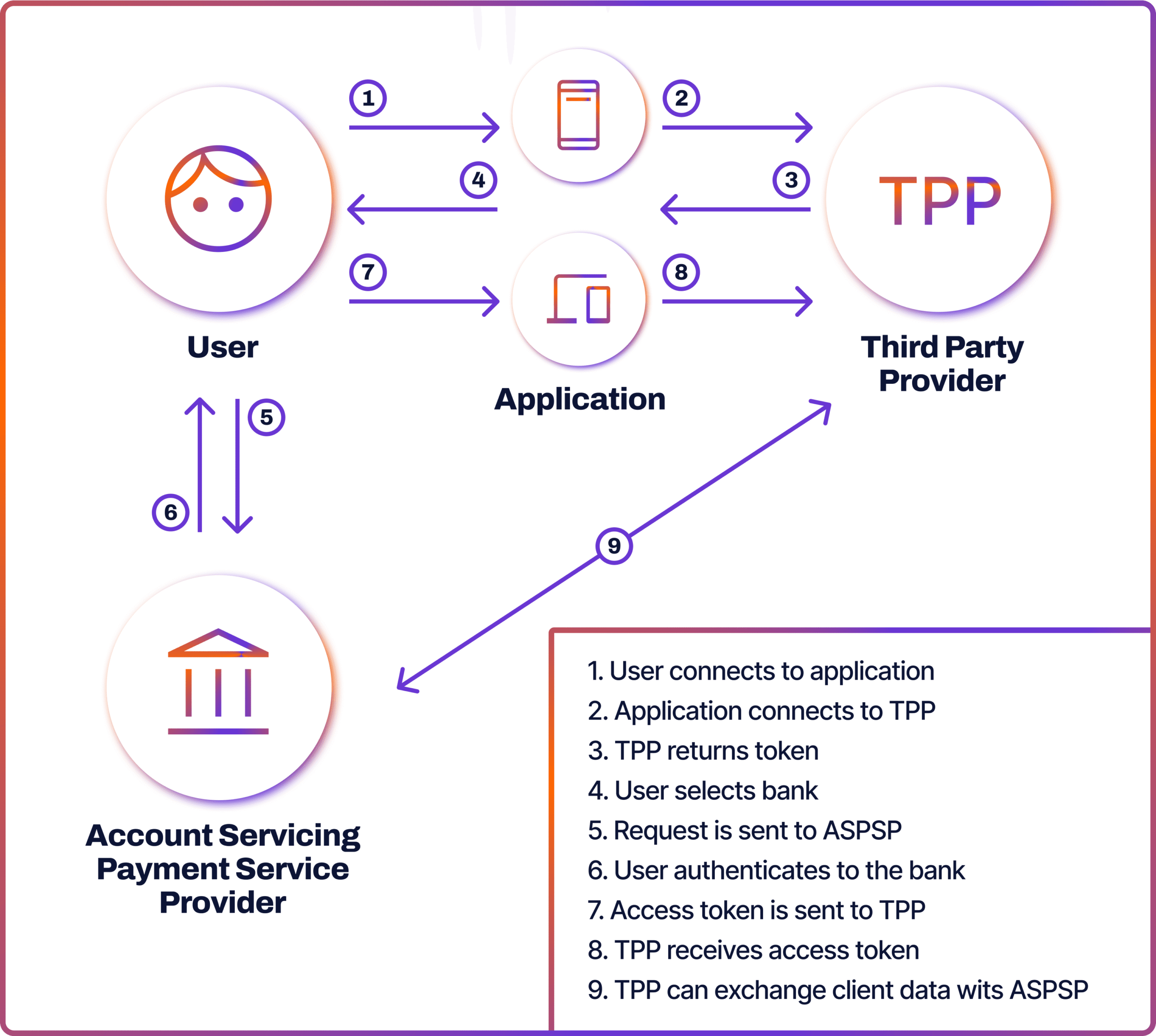

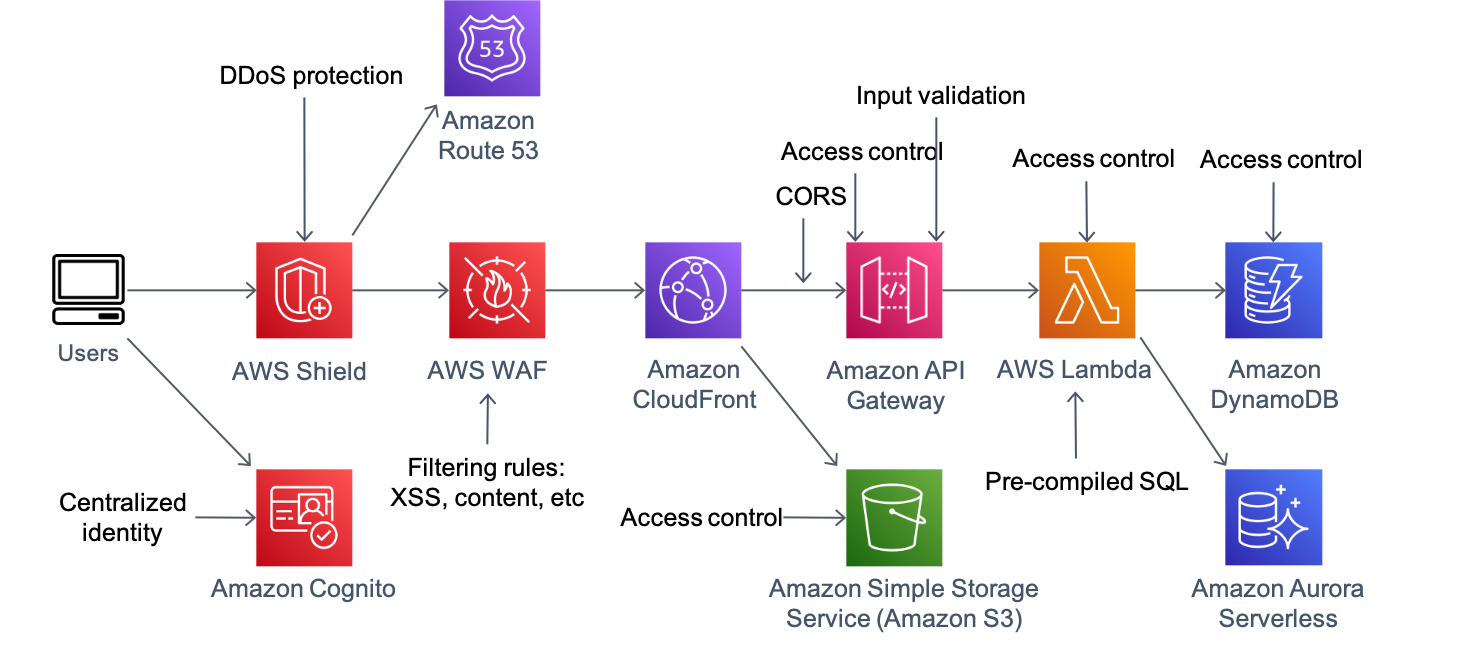

Open banking shifted the payments platform from a closed system to an external-facing ecosystem. Instead of serving only internal products and channels, payment capabilities needed to be safely exposed to third-party providers operating under their own business models, timelines, and technical constraints.

This introduced a different kind of complexity. Every API became a contract, every integration carried regulatory implications, and every design decision had to assume it would be used in ways the original team didn’t fully control.

Context and Scale

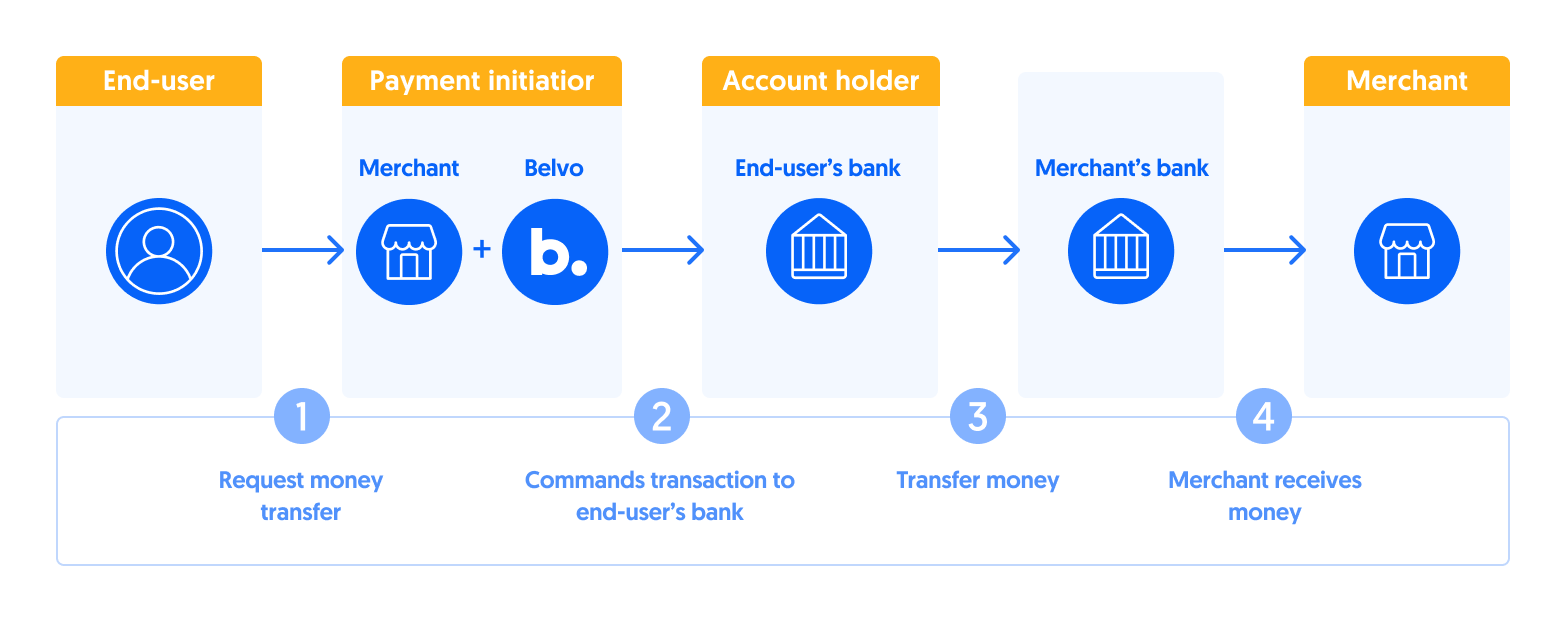

The platform supported third-party payment providers accessing account and payment capabilities through regulated interfaces.

These integrations operated at production scale, handling real customer funds and sensitive data, while being subject to strict consent, authentication, and audit requirements. Unlike internal consumers, third parties varied widely in maturity, technical capability, and use cases.

Failures here were not isolated. A poorly designed API or unclear consent model could impact customers, partners, regulators, and internal operations simultaneously.

The Problem

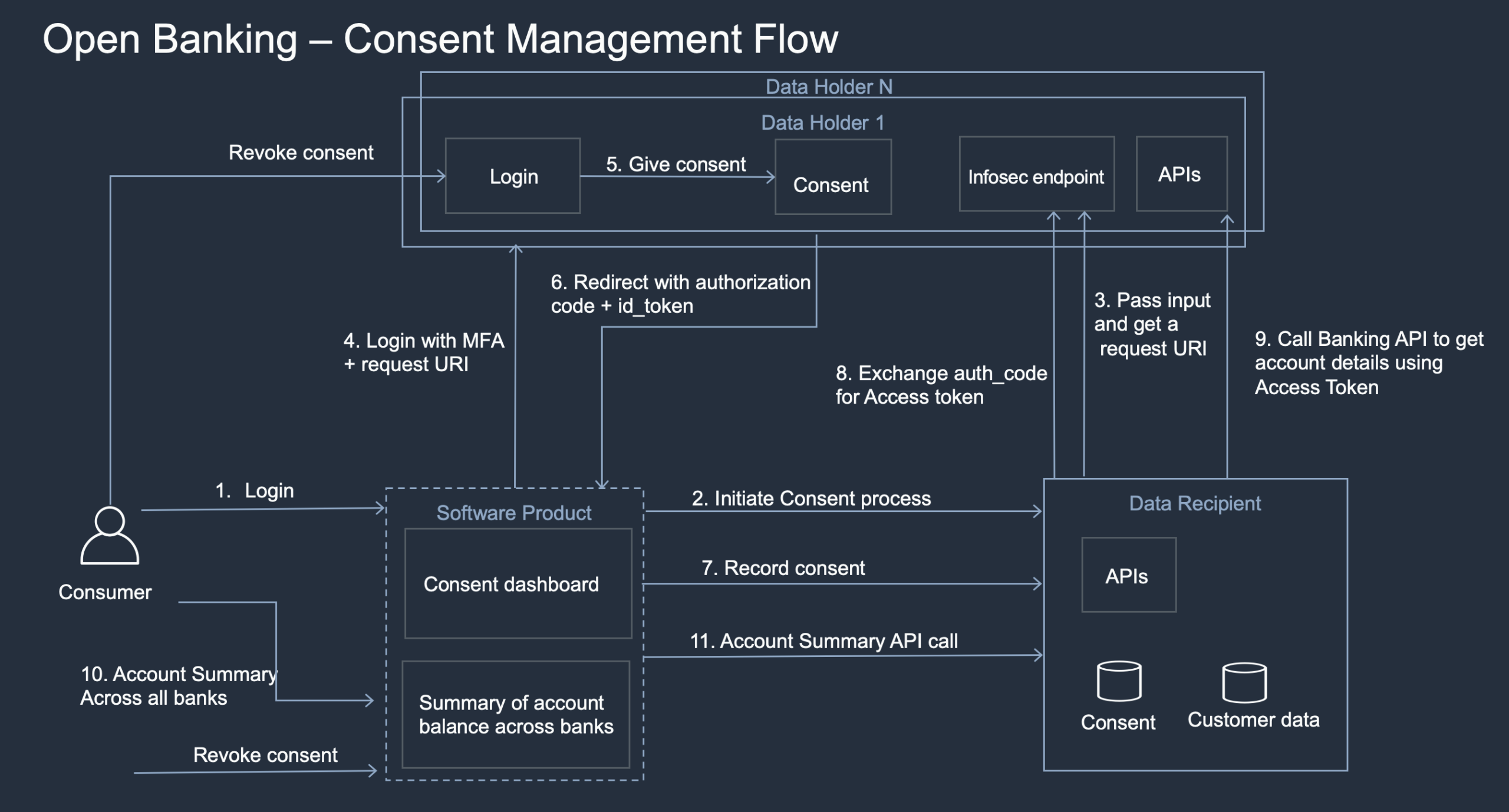

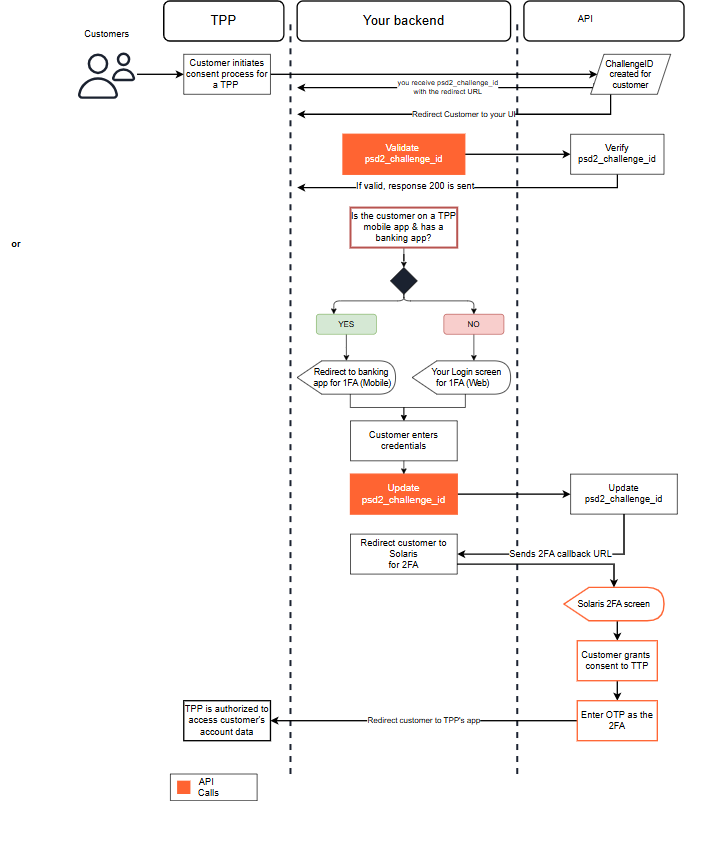

As open banking requirements expanded, existing internal APIs were not suitable for external use.

They lacked clear versioning, explicit consent boundaries, and consistent behavior guarantees. Regulatory expectations around customer authorization, data minimization, and auditability also raised the bar for how access needed to be controlled and monitored.

The core challenge was enabling third-party innovation without compromising customer trust, platform security, or regulatory confidence while avoiding a proliferation of bespoke integrations that would be costly to maintain.

My Role

I was responsible for shaping how payment and account capabilities were exposed to third parties through open banking APIs.

That meant working across product, security, compliance, and engineering to define what should be exposed, under what conditions, and with what guarantees. I focused on designing APIs that were stable, well-scoped, and aligned with regulatory intent, rather than simply mirroring internal interfaces.

A significant part of the role involved balancing openness with control. This included defining consent models, access scopes, and lifecycle behavior in ways that were understandable to third-party developers while remaining defensible to compliance and audit teams.

Decisions

One key decision was to treat open banking APIs as a product surface, not just a compliance obligation. This drove clearer documentation, versioning discipline, and predictable behavior for external consumers.

Another was being deliberate about scope. Rather than exposing broad internal capabilities, APIs were narrowly defined around supported use cases, reducing security risk and long-term maintenance burden.

There were also tradeoffs around partner onboarding. Automation and self-service were prioritized where possible, but not at the expense of oversight in higher-risk scenarios. This avoided creating an ecosystem that scaled faster than it could be safely governed.

Risks

Open ecosystems amplify risk.

Overly permissive access could expose customer data or funds. Overly restrictive designs could push partners toward brittle workarounds. Ambiguous consent flows could erode trust and attract regulatory attention.

Managing these risks required being explicit about boundaries, assumptions, and failure modes and resisting pressure to “just expose it” without understanding downstream impact.

Outcomes

Third-party payment providers were able to integrate through clearly defined, regulated interfaces rather than bespoke connections. Consent and access behavior became more consistent and auditable, improving confidence across security, compliance, and operations teams.

Internally, the platform moved toward a more intentional model for external access, reducing ad hoc integrations and creating a foundation that could evolve as open banking use cases expanded.