Users

Sales Representatives, Channel Partners, Finance & Sales Operations Teams

Industry

B2B Incentives / Payments

Product Stage

Scaled, Incentive Payout Platform

SPIFF Payments via Prepaid & Virtual Card Programs

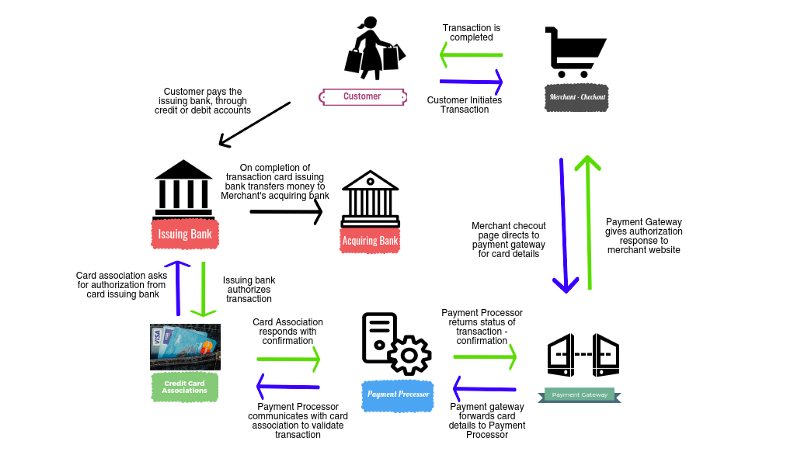

SPIFF payments introduced a different kind of incentive problem. Unlike rebates or reimbursements, SPIFFs required fast, tangible rewards that sales teams could feel immediately without creating accounting complexity or operational drag.

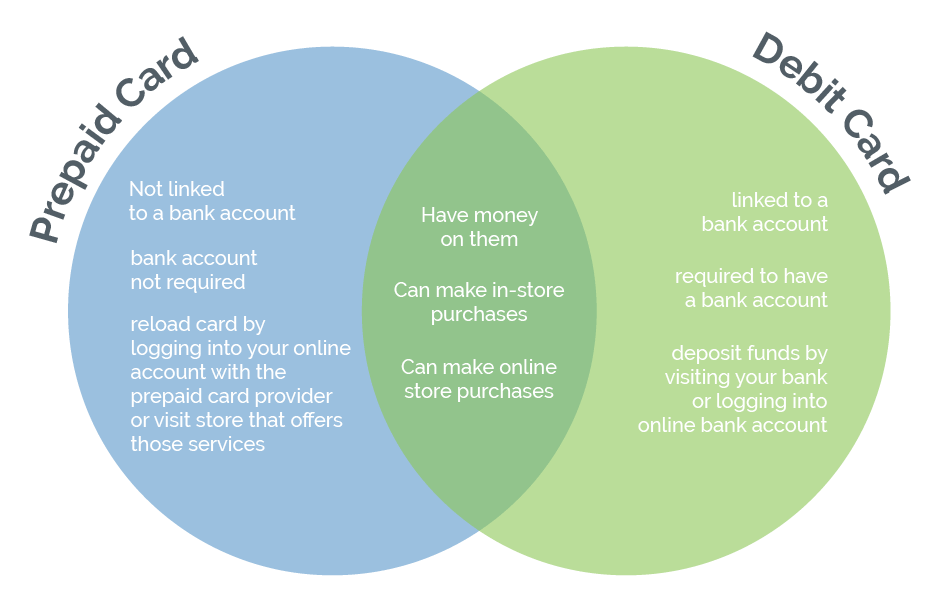

Delivering that experience meant integrating incentive payouts into prepaid and virtual card programs, supporting both reloadable and non-reloadable cards, while maintaining control over eligibility, funding, and reconciliation. The product had to balance speed and simplicity for recipients with financial rigor and auditability for the business.

Context and Scale

SPIFF programs were typically high-frequency and time-sensitive, tied to sales performance windows, promotions, or product launches.

Recipients expected rewards to arrive quickly and be easy to use. Internally, finance and operations teams needed assurance that funds were issued accurately, tracked correctly, and reconciled cleanly across payout cycles.

Because these programs touched external payment rails and third-party fulfillment systems, failures were highly visible, delayed payouts or incorrect amounts immediately undermined trust in the incentive program.

The Problem

Existing incentive mechanisms were too slow and operationally heavy for SPIFF use cases.

Manual payouts and delayed reimbursements failed to motivate real-time sales behavior. At the same time, simply issuing prepaid cards without controls introduced risk around overpayment, reconciliation gaps, and limited visibility into program spend.

The challenge was enabling fast, flexible SPIFF payouts while preserving financial control, traceability, and program governance without turning incentive delivery into a bespoke operational process.

My Role

I was responsible for shaping SPIFF payouts as a repeatable product capability, not a one-off integration.

That meant defining how incentive eligibility translated into card issuance, how different card types were supported, and how funding, activation, and usage were tracked across the lifecycle. I worked closely with engineering, finance, and operations teams to ensure payout flows aligned with internal controls while remaining simple for recipients.

A key part of the role was deciding where flexibility was appropriate and where guardrails were required particularly around reloadable versus non-reloadable cards, payout timing, and reconciliation behavior.

Decisions

One important decision was to support multiple payout models within a single product surface. Reloadable cards were treated as ongoing incentive vehicles tied to longer-running programs, while non-reloadable cards were optimized for short-term promotions and one-time rewards.

Another was separating reward issuance from funding and reconciliation. This allowed SPIFFs to be delivered quickly to recipients while ensuring financial systems remained accurate and auditable over time.

There were also deliberate tradeoffs around user experience versus control. Rather than exposing unnecessary complexity to recipients, controls were enforced upstream in program configuration and eligibility logic, keeping the payout experience simple without weakening governance.

Risks

SPIFF programs can fail loudly.

Delayed payouts erode trust. Incorrect funding creates financial exposure. Poor reconciliation leads to disputes and manual clean-up that quickly outweigh the value of the incentive itself.

Managing these risks required clear lifecycle ownership from eligibility through payout, usage, and reconciliation and resisting shortcuts that would compromise long-term operability.

Go-To-Market

The go-to-market approach focused on speed-to-value and behavioral impact, not payment mechanics.

Initial rollout targeted sales incentive programs where immediacy mattered most and existing payout methods were clearly ineffective. These programs were positioned around rapid reward delivery, with prepaid and virtual cards framed as tools to reinforce sales behavior in near real time.

Adoption was driven by program-level defaults rather than optional features. Once a SPIFF program was configured to use card-based payouts, that method became the standard path, eliminating manual alternatives and ensuring consistent execution.

Monetization scaled with program volume and frequency. As SPIFF usage increased, the platform captured value by reducing operational overhead, improving sales engagement, and enabling incentive programs that would not have been viable with slower payout mechanisms.

Outcomes

SPIFF payouts became faster, more predictable, and easier to operate at scale. Sales teams received timely rewards that reinforced desired behaviors, while finance and operations teams retained visibility and control over incentive spend.

The platform was able to support both short-term promotions and longer-running incentive programs without fragmenting payout logic or increasing reconciliation burden.