Users

Payments Strategy Teams, Risk Management Teams, Fraud & Compliance Teams, Authorization Platform Engineering

Industry

Banking / Payments / FinTech

Product Stage

Production-Grade AI Decision Optimization Platform (Internal, Risk-Critical)

Authorization Strategy Optimization (AI-Based)

In high-volume payment systems, authorization decisions are rarely static. Approval rates, fraud exposure, customer experience, and network performance all shift continuously based on geography, merchant behavior, customer segments, and evolving payment patterns.

This product focused on building an AI-assisted authorization strategy optimization layer that helped continuously tune approval logic not by replacing real-time decisioning, but by learning from outcomes and recommending better strategies over time.

The objective was to increase approvals and revenue without increasing fraud or operational risk.

Context and Scope

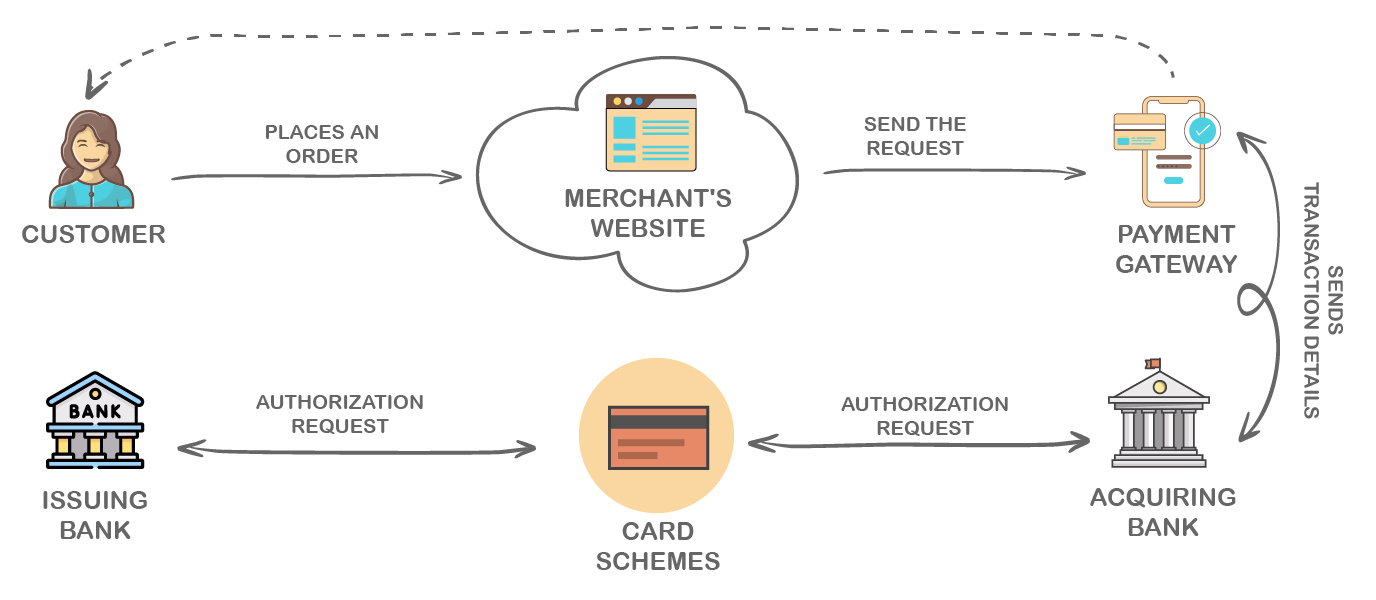

The authorization platform operated at global scale, processing card transactions across multiple networks, markets, and merchant categories.

Authorization logic relied on a combination of network rules, internal risk thresholds, customer profiles, and merchant-specific strategies. While effective, these strategies were often tuned manually, based on historical reports, lagging indicators, and periodic reviews.

As transaction patterns evolved, driven by new merchant models, cross-border growth, and digital wallets, static strategies struggled to keep pace. Small misconfigurations could materially impact approval rates or customer friction at scale.

The Problem

Authorization strategies were reactive.

Teams relied on after-the-fact analysis to identify declines that could have been approved or approvals that carried unnecessary risk. Adjustments were slow, conservative, and often applied broadly rather than contextually.

The core problem was designing a system that could:

-

Learn from historical authorization outcomes

-

Simulate alternative strategies safely

-

Recommend targeted adjustments by segment

-

Balance revenue uplift against risk exposure

This required decision optimization, not real-time classification.

My Role

I owned the product strategy for the authorization strategy optimization capability.

That included defining optimization objectives, determining which dimensions were safe to tune algorithmically, and designing how recommendations would be surfaced to risk and payments teams.

I worked closely with risk, compliance, and engineering stakeholders to establish clear boundaries: what the system could recommend, what required human approval, and what should remain fully deterministic.

A critical part of my role was ensuring AI recommendations aligned with regulatory expectations around explainability, governance, and accountability.

Optimization Approach & Product Decisions

Rather than optimizing individual transactions, the system operated at the strategy level.

Historical authorization data was analyzed to identify patterns where alternative thresholds, rule ordering, or network preferences could have improved outcomes. The system modeled tradeoffs across approval rate, fraud rate, and customer experience, surfacing recommendations with clear impact estimates.

AI was used to prioritize opportunities and simulate outcomes not to directly approve or decline transactions. This kept the optimization layer advisory, explainable, and controllable.

Recommendations were contextual, scoped to specific merchants, corridors, customer segments, or transaction types, avoiding one size fits all changes.

Managing Risk & Regulatory Constraints

Authorization optimization carries inherent risk.

Over aggressive strategies can increase fraud. Overly conservative ones reduce revenue and frustrate customers. Automated changes without oversight would be unacceptable in a regulated environment.

To manage this, all recommendations were:

-

Confidence-scored

-

Impact-estimated

-

Human-reviewed before activation

Changes were applied incrementally and monitored closely, with rollback mechanisms in place.

This ensured the system improved outcomes without undermining trust or governance.

Go-To-Market

The optimization capability was introduced as an internal decision-support platform.

Rather than positioning it as AI-driven automation, it was framed as a way to focus human expertise where it mattered most, highlighting the highest impact opportunities for improvement.

Adoption was driven through pilot programs with risk and payments teams, demonstrating measurable approval uplift without increases in fraud.

Outcomes

Authorization strategies became more adaptive and data-driven.

Teams were able to identify and implement targeted optimizations faster, improving approval rates while maintaining risk controls. Manual analysis effort decreased, and strategy reviews shifted from retrospective reporting to forward-looking decision-making.

Most importantly, the platform helped align risk and revenue objectives, making tradeoffs explicit rather than implicit.