Users

Cardholders, Merchants, Risk & Operations Teams

Industry

Financial Services / Payments

Product Stage

Scaled, AI-Assisted Risk Platform

Fraud Detection & Risk Signals (AI-Assisted)

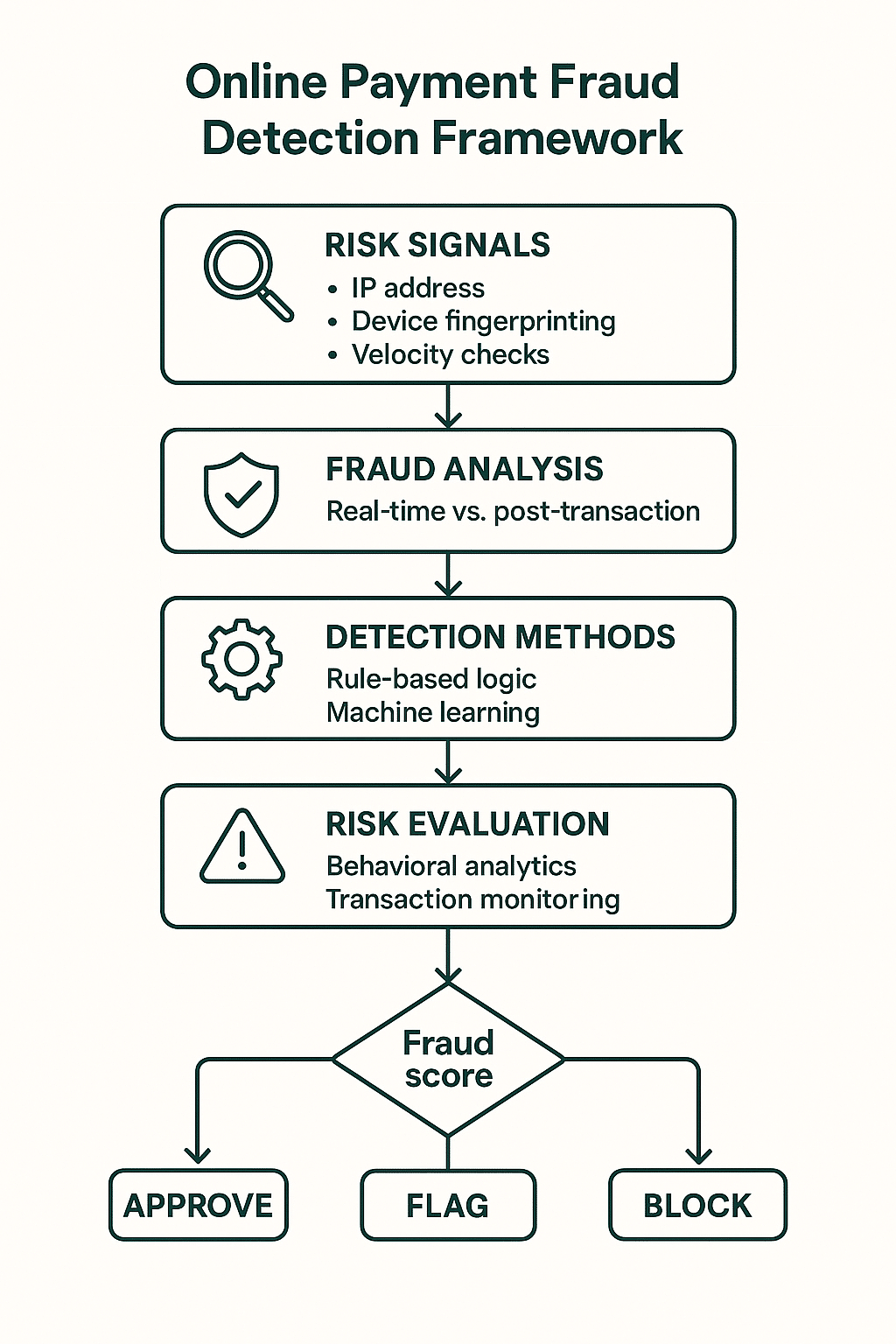

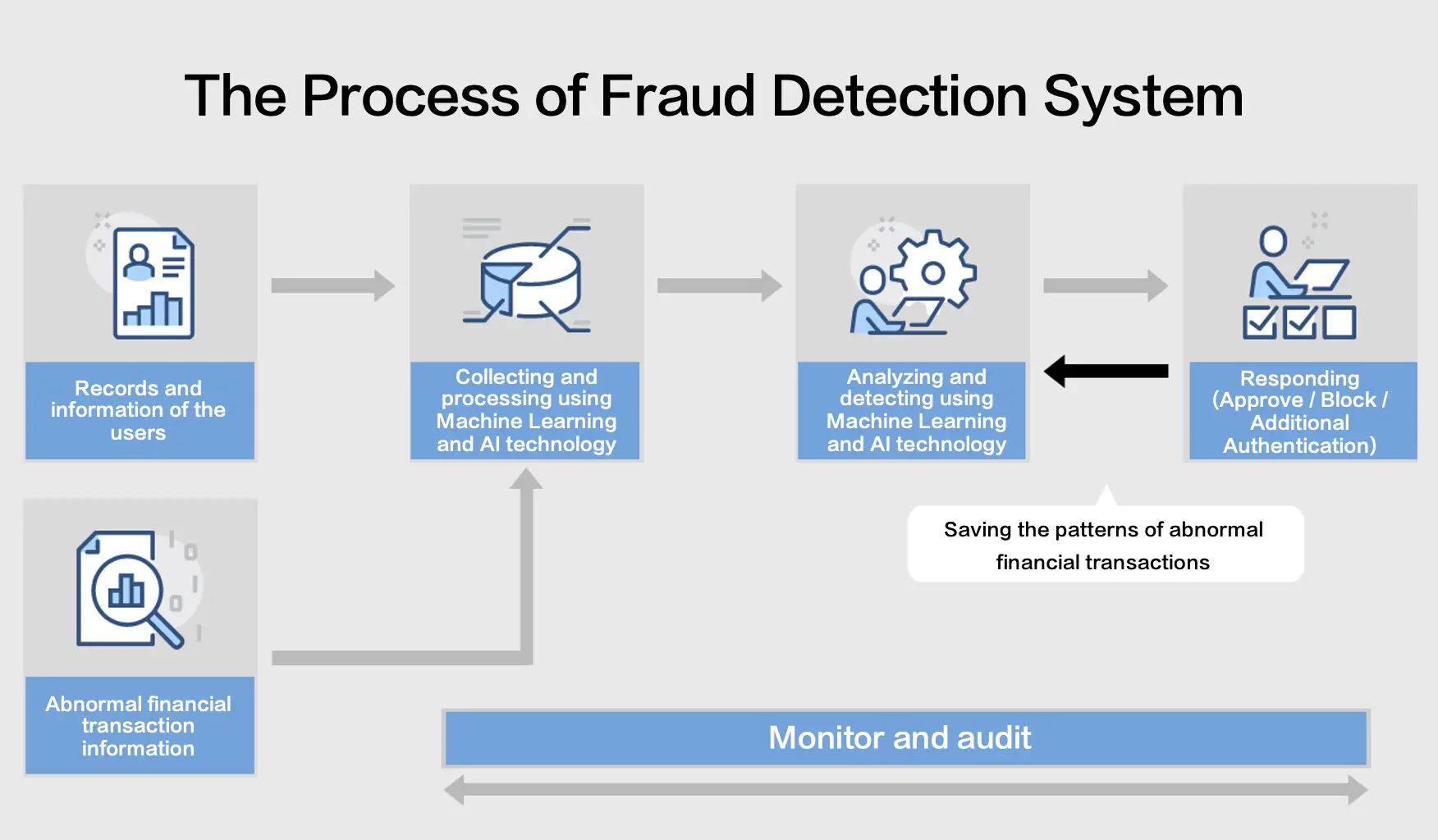

Fraud detection and risk decisioning sat alongside the core payment flows, influencing whether transactions were approved, challenged, or declined in real time. Unlike deterministic rules, this system relied on a combination of behavioral signals, historical patterns, and contextual data to assess risk under uncertainty.

The challenge was not simply detecting fraud, but doing so in a way that balanced customer experience, approval rates, and operational trust. Every risk decision carried consequences like a false positive could block a legitimate purchase, while a false negative could expose the platform to financial loss and regulatory scrutiny.

Context and Scale

The risk system operated at transaction scale, evaluating signals across millions of payment attempts and feeding into authorization decisions that had to complete within tight latency budgets.

It served multiple stakeholders simultaneously. Customers experienced the outcome at checkout. Risk and operations teams depended on consistent, explainable decisions to manage fraud and disputes. Compliance teams needed confidence that decisioning logic was defensible and auditable.

Risk models and signals were constantly evolving, but the system itself had to remain predictable, stable, and trusted.

The Problem

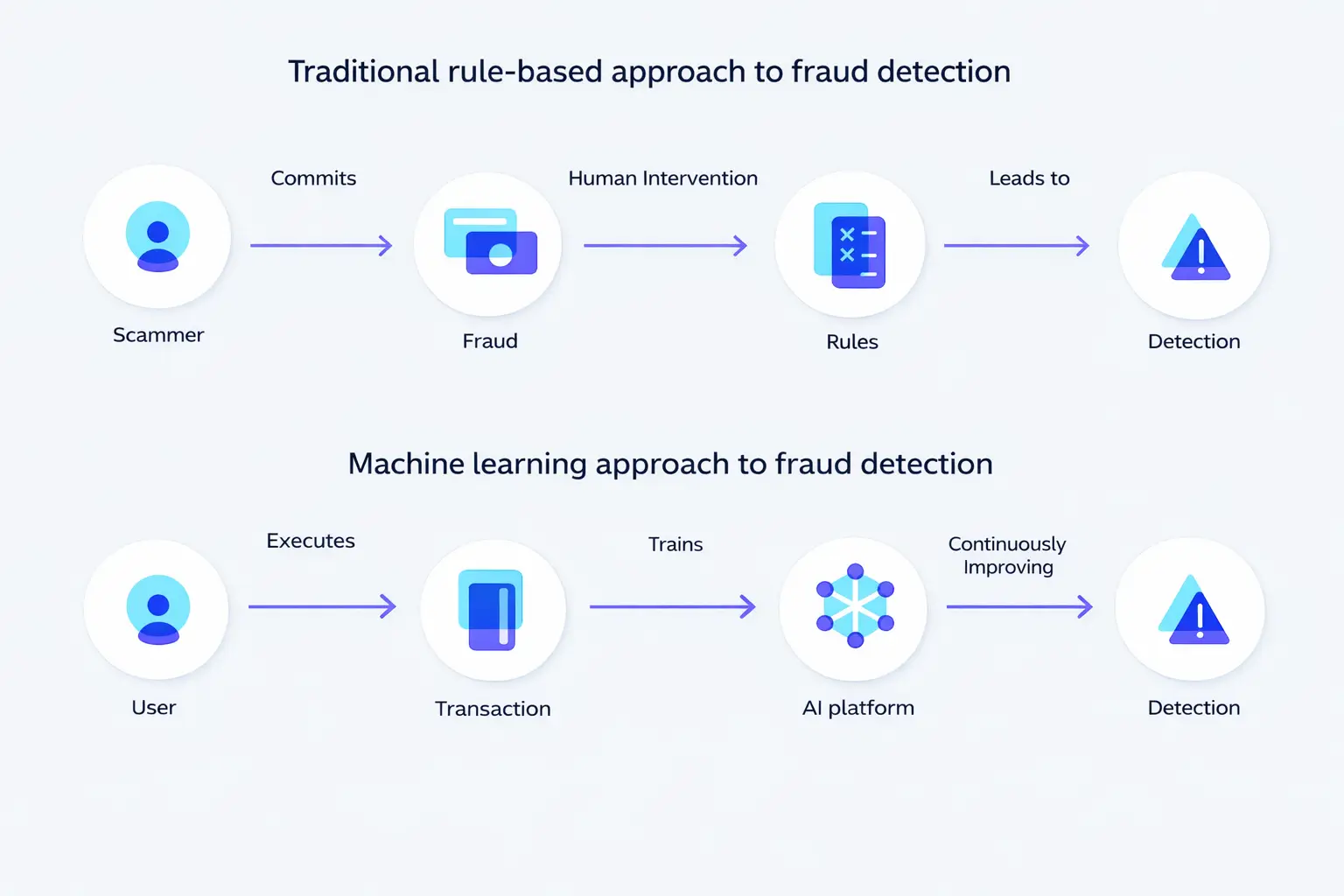

As payment volume and complexity increased, existing risk approaches began to show limitations.

New payment methods, tokenized transactions, and BNPL flows introduced behaviors that didn’t always fit neatly into existing rule-based logic. Fraud patterns adapted quickly, while overly aggressive controls created customer friction and operational noise.

The core problem was not a lack of signals, but deciding how to use them responsibly. Risk decisions needed to be accurate, timely, and explainable, without turning the authorization flow into a black box that teams struggled to reason about or control.

My Role

I was responsible for how fraud detection and risk signals were incorporated into real-time payment decisioning.

That meant shaping how signals were introduced, evaluated, and acted upon within authorization flows, rather than treating risk as a separate, downstream concern. I worked closely with risk, data, and engineering teams to define where probabilistic decisioning made sense, where deterministic controls were still required, and how the two could coexist without creating unpredictable outcomes.

A significant part of the role involved translating model outputs into product decisions that were operable at scale. This included aligning on thresholds, escalation paths, and fallback behavior when confidence was low or signals were incomplete. The goal was not maximum model sophistication, but decisions that teams could trust and customers could live with.

Decisions

One key decision was to avoid pushing AI-driven risk decisions blindly into every transaction path. Instead, probabilistic signals were applied selectively, augmenting existing authorization logic rather than replacing it outright. This reduced the risk of systemic behavior changes that would be difficult to diagnose or reverse.

Another decision centered on explainability. Risk outputs were structured so that downstream teams could understand why a transaction was flagged, not just that it was. This reduced operational friction and made it easier to respond to disputes, audits, and customer complaints.

There were also tradeoffs between sensitivity and stability. Rather than continuously tuning models in production, changes were introduced deliberately, with clear evaluation windows, to prevent oscillating behavior that could confuse both customers and internal teams.

Risks

Fraud systems fail in subtle ways.

Overly aggressive risk controls can quietly erode approval rates and customer trust. Under-tuned systems can allow losses to accumulate before patterns are obvious. Black-box decisioning can leave operations and compliance teams unable to defend outcomes when challenged.

Managing these risks required discipline around where automation was appropriate, how much autonomy models were given, and how human oversight remained part of the system.

Outcomes

Risk decisioning became more adaptive without becoming opaque. Fraud signals were incorporated in ways that improved decision quality while preserving predictable authorization behavior. Operational teams gained clearer insight into why transactions were flagged, and changes to risk logic became easier to reason about and manage.

The platform was able to support newer payment flows and higher volumes without relying solely on static rules or overcorrecting in response to emerging fraud patterns.