Improving Authorization Outcomes Through AI-Driven Strategy Optimization

Context

The authorization platform was already operating at significant scale, handling millions of card transactions daily across multiple channels and markets. Approval decisions were being made in real time under strict latency requirements and regulatory scrutiny. While the system was stable, approval rates had plateaued, and there was growing pressure from commercial and digital teams to improve customer experience without increasing fraud exposure or regulatory risk.

At the same time, fraud controls had become increasingly conservative over time. New rules were regularly added to mitigate emerging threats, but very few were ever retired. This resulted in overlapping signals, inconsistent outcomes across segments, and limited visibility into why transactions were being declined. Stakeholders knew value was being left on the table, but there was little confidence that changes could be made safely at scale.

My Role

I owned the authorization strategy layer end to end, with responsibility spanning decision logic, risk alignment, and performance outcomes. My role sat between fraud, engineering, data science, and commercial stakeholders, ensuring that strategy changes balanced approval rates, fraud losses, latency, and regulatory expectations.

Beyond delivery, I was accountable for how decisions were governed, rolled out, monitored, and explained. This included setting the operating cadence for strategy changes, defining safety thresholds, aligning on risk tolerances, and ensuring leadership had confidence in both the outcomes and the controls behind them.

The approach

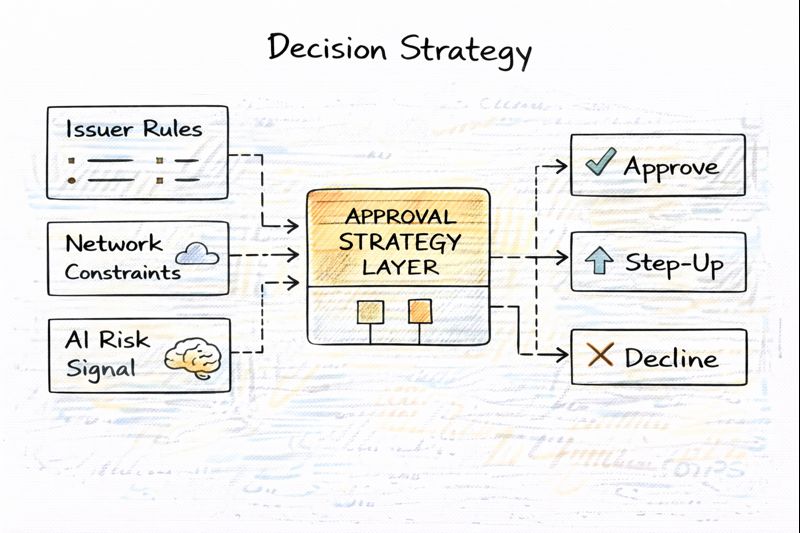

1. Reframing authorization as a strategy optimization problem, not a rules problem

Instead of treating declines as isolated rule failures, I reframed authorization as a portfolio of decision strategies operating under shared constraints. The goal was no longer to block fraud more aggressively, but to maximize approved, low-risk volume within clearly defined loss and latency budgets. This shift helped align fraud, product, and commercial teams around a common objective rather than competing incentives.

2. Introducing AI-assisted decision optimization, not black-box automation

Rather than replacing existing controls, we layered AI-assisted models alongside them to score transactions and evaluate the effectiveness of existing rules. These models surfaced patterns where declines were consistently low-risk or where multiple signals were redundantly blocking the same transactions. The emphasis was on decision support and optimization, not autonomous approvals.

3. Segmenting strategies by risk and context

Authorization behavior was redesigned to vary by transaction context, customer tenure, channel, and spend profile. Low-risk segments were allowed more flexible strategies, while high-risk paths remained tightly controlled. This reduced false declines without weakening protection where it mattered most.

4. Embedding explainability into strategy decisions

For every AI-assisted recommendation, we required a clear explanation of which signals influenced the decision and how it aligned with risk policy. This was critical for building trust with fraud leadership, compliance teams, and regulators, and it allowed strategy changes to move forward without prolonged escalation cycles.

5. Shipping behind controls with continuous validation

All strategy changes were deployed behind feature flags and approval thresholds. Performance was monitored in near real time, with explicit rollback criteria defined before launch. This allowed us to iterate safely and build momentum without creating fear around experimentation.

Trade-offs and hard calls

One of the hardest decisions was accepting that improving approval rates would inevitably surface some increase in fraud attempts, even if net losses remained flat. I worked with risk leadership to define acceptable loss corridors rather than absolute zero-tolerance thresholds, which required a shift in mindset.

Another trade-off involved explainability versus model sophistication. Some higher-performing models were intentionally deprioritized because their decision logic could not be explained clearly enough to satisfy regulatory and internal governance requirements. Choosing slower, more transparent progress over aggressive optimization was a conscious leadership call to ensure long-term sustainability.

Operating model

Authorization strategy operated on quarterly themes aligned to business priorities, such as improving digital wallet approvals or reducing false declines in cross-border transactions. Within each quarter, changes were reviewed bi-weekly through a formal strategy forum that included product, fraud, data science, and engineering leads.

Material changes required documented risk sign-off, defined success metrics, and pre-approved rollback plans. This operating model allowed us to move faster over time while maintaining a strong control posture and reducing stakeholder friction.

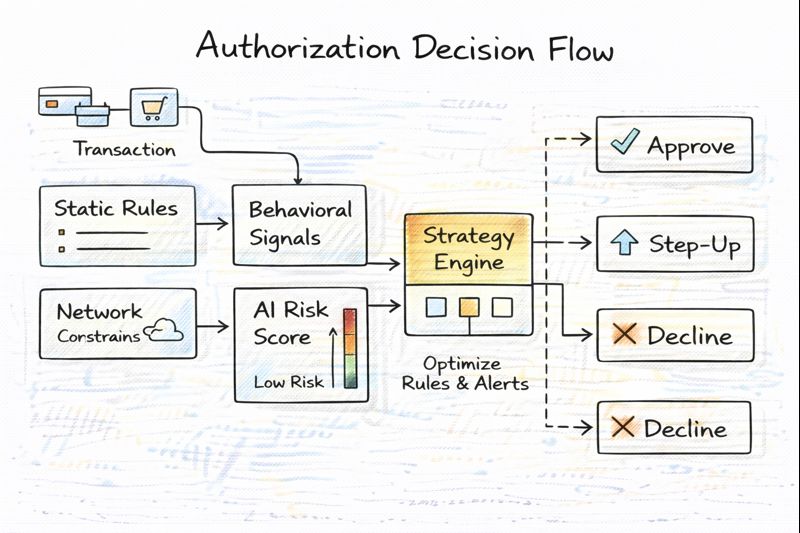

Architecture narrative

The AI-assisted optimization layer sat alongside the existing rules engine rather than replacing it. Transaction requests flowed through a pre-screening layer, followed by AI scoring and contextual enrichment. Based on the combined output, the authorization strategy selected an approval, decline, or fallback path.

Critical dependencies were isolated with strict timeout policies. If AI services were unavailable or exceeded latency budgets, decisions defaulted to the baseline rule set. This ensured system resilience and prevented AI from becoming a single point of failure in the authorization flow.

Outcomes

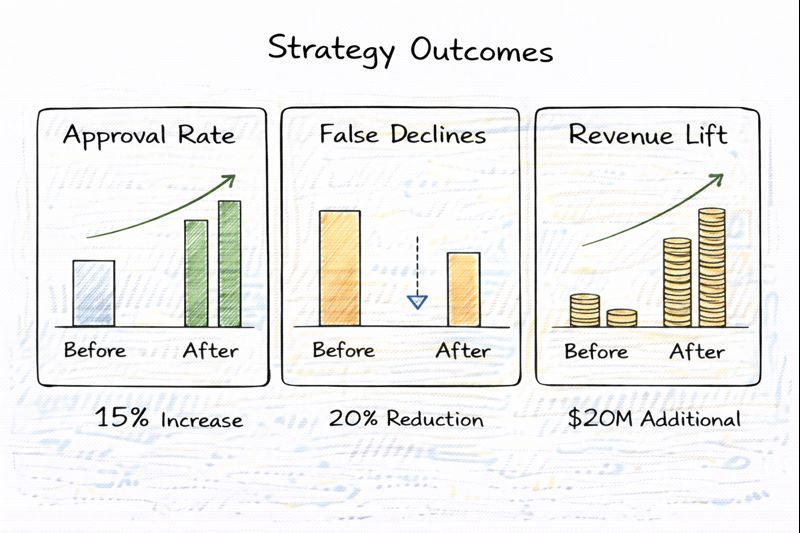

Within the first two quarters, approval rates improved by approximately 2–3 percentage points in targeted segments, translating into meaningful incremental revenue without a corresponding increase in fraud losses. False declines were reduced most significantly in recurring customer and digital wallet transactions, where prior controls had been overly conservative.

Equally important, stakeholder confidence improved. Fraud and compliance teams gained better visibility into why decisions were being made, and leadership had clearer insight into how approval rate improvements mapped to risk exposure. The platform moved from reactive rule management to proactive, data-driven strategy optimization.